Mortgages in Germany explained

Market News

Rent or Buy in 2026? Does Buying Still Make Sense?

Read moreProperty Search

Where It Still Makes Sense to Buy a Home in Germany – 2026

Read moreMortgage Advanced

Cash-Out Mortgage: How to Unlock Wealth from Your Existing Property in Germany?

Read moreMarket News

Our German Housing Outlook (2025)

Read more

Mortgage Fundamentals

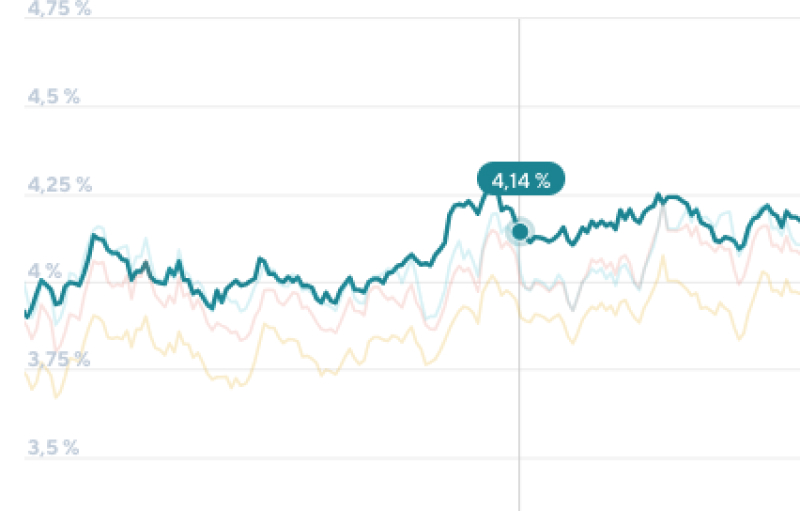

What Are the Current Mortgage Interest Rates in Germany and How Do They Evolve?

Read more

Mortgage Fundamentals

How to refinance your German mortgage?

Read more

Mortgage Advanced

KfW 40 QNG: The Comprehensive Guide to Subsidies, Costs, and Requirements

Read more

Homebuying Basics