Buying a new build in Germany

Nothing can go wrong with a new build? It's not quite that simple. There are pitfalls waiting here, too. We explain what you need to consider.Updated on July 15, 2025

However, there are a few things to consider when buying a new build in Germany — especially if the construction is still under development. This also applies to home financing. In this article, we explain what you need to know about buying a new build.

Buying a new build from a German developer

You usually buy a new apartment or a new house directly from the builder or the project developer. The advantage of this is that, in most cases, you save the commission for the real estate agent. This has a positive effect on the purchase costs, and the price can also be more competitive. The German developer takes over the complete planning and supervises the implementation of the construction.

When you buy early, you often get some benefits, as project developers want to show buyers that their project is successful. Prices can be lower, either outright or because you can choose the better views and layouts for the same cost. Often, when a certain round percentage of apartments or houses is sold, the developer raises the price.

Buying a new building in Germany before completion — know the risks

When the housing market is competitive, and there is a shortage of new apartments, properties are sold out completely before the building project is even completed. In that case, there may not even a model home to visit. The customer can only see a mock-up, a scale model of the house or apartment, and the architect's plans and designs, and must then decide on that basis for or against the purchase. So, practice reading the drawings. Try to infer where sunlight will come in. and at what time. Check the ceiling height and window height!

There are also building risks involved. Buyers may have a hard time assessing the building materials and how thoroughly the construction work will be done. Mistakes must be corrected afterward, so make sure the contract provides for that. Be prepared to face delays! In the case of an old building, a surveyor can make a good estimate of the structure and expected costs.

Of course, a new building also has huge advantages, like having high energy efficiency, much lower maintenance cost, modern equipment, efficient layouts, and often larger windows.

Reading tip: 4 mistakes you should avoid with your mortgage.

Buying from a German real estate developer

To protect yourself as much as possible, pay attention to the following points. These are also explicitly recommended by homeowners' associations.

Have the developer send you the building and service description at least 14 days before the notarization, and go through it carefully. If you are unsure, have it additionally checked by an expert, such as a lawyer for real estate law.

Have the purchase contract sent to you at least 14 days before notarization and check it carefully. Pay particular attention to whether and how the construction and service descriptions are included. The 14-day period is regulated by law (§ 17 Absatz 2 Satz 2a BeurkG). You are entitled to receive the contract at least two weeks before the day of the signing.

Check the declaration of division and the division plan carefully. Can the information also be found in the land register and purchase agreement?

Check the creditworthiness of the developer. Online insolvency databases will help you with that. It is best to have the developer show you additional reference projects that she has already realized. This helps you check her reliability.

The payment should not be made all at once but according to the progress of the construction work. If a construction phase is completed, the developer receives a part of the purchase price.

An independent building inspection, for example, by TÜV or Dekra, is an advantage for you. Find out whether the developer is planning this.

Bring your own building consultant or surveyor to the final inspection to directly record any defects.

Special requests or your own contributions must be recorded in the developer contract.

You should also contractually stipulate that you will receive all relevant documents, such as the soil survey, the energy certificate, building application plans, etc. when construction actually begins. After all, as a buyer, you are not only buying an apartment, but you are part of the entire residential complex.

Take care of the length of your warranty. For some developers, this is a negotiable point.

Make sure that the developer has a building permit--indeed, sometimes they don't--and that the extract from the land register is up-to-date.

Check the neighborhood and building site to get a better idea of your future home.

In the contract, there should be a special clause that clarifies a penalty for building delays. You can negotiate a sum per day per square meter, or the developer has to pay you the damage that occurred (e.g., rent for a flat because you can't move in your property and commitment fees from the bank).

Financing of a new build in Germany

Unlike with an existing building, you do not pay the purchase price all at once but in installments. You agree with the seller on when what amount is due. Usually, the payment is divided according to construction phases.

This is good for both sides. The developer receives money based on actual work, and the buyer only pays if the building is actually progressing. This also protects you from the insolvency of the construction companies – since if they don't build, they don't get paid.

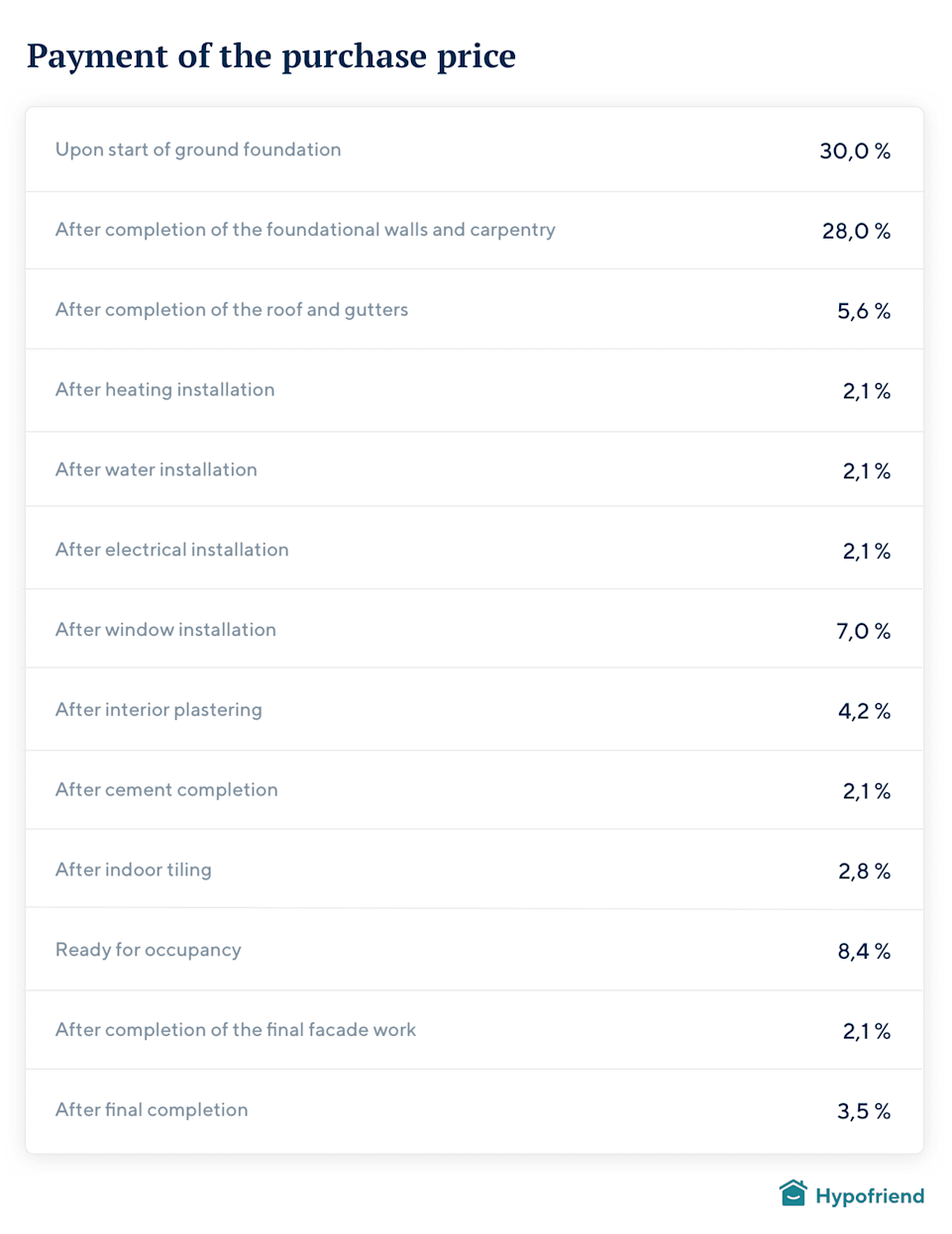

Payment plan

Payment by installments is a step-by-step business. If sections are completed, payment follows. How much of the purchase price is due and when is, in general, regulated by the Brokers' and Developers' Ordinance. Here, you will find an overview. The installments are also a matter of negotiation.

Consider commitment fees in your mortgage

Since you do not pay the purchase price all at once, you will want the bank to disburse the loan in installments, which they will do. However, if the bank lends you money, it cannot use it for any other purpose and, therefore, charges you a commitment fee on any money it expects to disburse but doesn't. Nearly all banks offer a commitment fee-free period. It is between six and 24 months. The fees also vary by bank.

Therefore, we have a detailed calculator that we can share with our customers. From our side, we use the tool to evaluate the overall cost for a customer, including the commitment fees, so that we can secure the best all-in deal. Customers can use the tool to help plan their cash flow. We both look at the possibility of delays and how that impacts the cost and the cash you need, as this often happens.

Note that the interest rate accrues and becomes payable monthly as the loan is disbursed. In other words, with each installment, your loan amount and interest payable increase. Therefore, for a time, you will have double payments: your current rent and the interest payment for your new home. Thus, planning your cash flow is important.

The good thing is that the principal only becomes due once the bank has paid out the full amount of the loan. So the repayment only starts at that point.

In any case, we hope that with this advice in your pocket, you can enjoy your home-buying journey and then your new home!

You can readmore about commitment fees here.