Notary Fees Calculator Germany

Use our calculator to find out how much the notary and land registry costs are for your property purchase and how the costs break down.

Available across Germany

Available across Germany

Free for you, paid by lenders

Mon - Fri: 9 AM - 7 PM

The total cost is 4.578 €, of which the cost for the notary is 3.127 € and for the land register 1.451 €.

Notary fee | 3.127 € |

|---|---|

Notarization of the land purchase contract | 1.570 € |

Notarization of the mortgage (Grundschuld) | 273 € |

Support fee for the purchase contract (Kaufvertrag) | 393 € |

Execution activities (Vollzugstätigkeiten) | 393 € |

VAT | 499 € |

Land register fee | 1.451 € |

|---|---|

Notice of conveyance (Auflassungsvormerkung) | 393 € |

Registration of the mortgage (Grundschuld) | 273 € |

Registration of the owner | 785 € |

In total, the cost is 1,12 % of the property price.

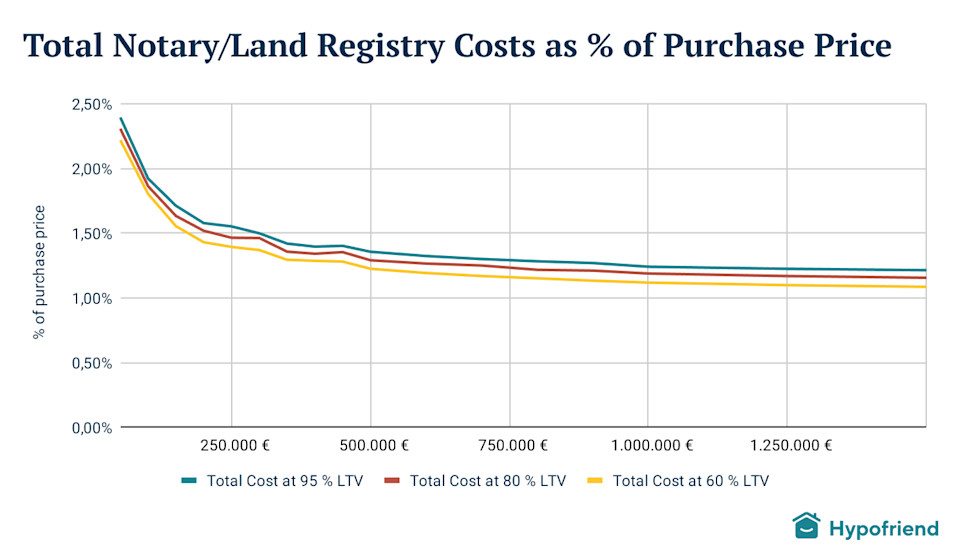

So typically, the cost is much less than 2 %. The graph below shows the bottom line for most buyers: a cost that is quite a bit less than 2 %. Note that LTV stands for the loan-to-purchase-price ratio:

As you can see in the graph, notary fees depend, in particular, on the size of the purchase and the size of the mortgage. Those with lower loans compared to the property price have significantly lower notary fees. In addition, those whose purchase price is low, have relatively high fees, and vice versa.

The good news is that for the typical city property buyer, the fees will be more like 1,3 % so you can save a good sum of money, especially compared to the 2 % standard estimate that banks use!

Calculate how much you can afford and get a free online mortgage recommendation in only a few clicks.

See my optionsNotary fees are non-negotiable in Germany, but you can avoid extras

Unfortunately for you, notary fees in Germany are tightly regulated (in the Court and Notary Costs Act), and you cannot negotiate the fees or shop around.

You can, however, save by sticking to the basic needs as estimated above and avoiding the extras.

The main extras you can avoid are:

The use of a so-called “Notaranderkonto”, which is a third-party notary account and a clean and safe way to transfer money to the seller while you are waiting for the keys. In Germany, you don't need to do this. In Germany, buyers simply instruct their mortgage bank to pay the seller directly, as the notary has already preliminary registered you and the bank in the Grundbuch. This is safe. If you would use the “Notaranderkonto”, you would have to pay the notary close to 1.000 €, for a house of 500.000 €.

You can also avoid paying up to 250 € if the Notary does not use specially structured files for the contracts (“Vollzugsgebühr für die Erzeugung von strukturierten Daten”). Be sure to ask your notary about their practice and suggest they avoid these fees. Typically, the notary makes quite a bit of margin on property transfer, so they should not mind.

Buyers wanting to speed up payment by their bank can ask the notary for a so-called confirmation by the notary (called “Notarbestätigung gegenüber der Bank” in German). In this way, the notary assures the bank that nothing stands in the way of creating a first-ranking land charge. This expense may be important if the seller is in a rush and you are afraid of losing the property. This will add a bit over 234 € for a loan of 450.000 €.

Once the loan amount giving rise to the land charge is fully paid off, the land charge in the land registry will not automatically be removed. This needs to be done at your request and will cost a few hundred Euros more if the act is drafted already by the Bank. However, instead of having it removed, the land charge can be reused for refinancing, so it makes sense just to leave it dormant until you sell the property. If it is a so-called “Briefgrundschuld,” it can also be passed on to another bank. This could, hence, save you the cost of having to enter the cost for a land charge again.

The de facto land charge can be augmented with land charge interest (15-20 % over the base land charge ordered) and auxiliary payments (5-10 % of the base land charge ordered). See for these terms and their use our detailed 10 steps guide on the notary process. The notary fees only reflect, however, the basic land charge, i.e., the size of the mortgage. From a cost perspective, you, therefore, do not need to be concerned about this.

© 2026 Hypofriend. We put a lot of work into creating original content for our readers. Therefore you are not permitted to reproduce our work or use it to train Al systems without quoting us as a source and adding a link.