Why Guaranteed German Pension Products Just Aren’t Worth It

Guarantees sound like a great thing - but we will show you that they can also be a bad idea, especially when it comes to pension products.

Dr. Chris Mulder

Published on Nov 27, 2022 . Updated a month ago

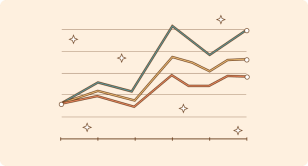

Insurance companies promote guaranteed pension products as being particularly rich in opportunity and value sure. Indeed, these products are rather popular, as they seem to offer the best of two worlds: participation in the upswing of a stock index, and the guarantee of never facing a loss. Unfortunately, as we show here with a close-up look at Index Select from industry leader Allianz, these claims are in fact rather misleading.

Our conclusion: Allianz Index Select and similar products¹ are in reality not the stock index participation strategies they are being billed as, but rather option arbitrage strategies. Such products are not suitable for long-term investors, given their high cost and low returns, and the uncertainty of whether even modest returns could hold up over the medium to long run. Figure 1 shows you the essence of the story: your money is stable but will not grow, unlike the index which is unstable but will grow.